Why Stocks Outperform Bonds

In 1999, James K. Glassman and Kevin Hasset (the current director of President Trump’s National Economic Council) published Dow 36,000, which predicted that the Dow Jones Industrial Average would reach 36,000 points by the year 2004. The prediction failed in spectacular fashion after the twin stock market crashes of the dot-com bubble (2000-02) and the financial crisis (2008). The Dow wouldn’t crest 36,000 until November 2, 2021, only 17 years too late.

The crux of Glassman and Hassett’s argument was that stocks were not risky in the long run and that the Equity Risk Premium (ERP) should therefore be close to (if not) zero. The ERP is the extra return above the “risk-free” rate (such as US Treasuries) that investors demand for holding equities. Dow 36,000 contends that stock valuations will rise as investors price in a lower ERP, meaning future returns after that point would be more bond-like.1

While their argument failed to pass the empirical test, the authors echoed a question asked by other scholars and economists: If the risk of equities in the long run—for example, 40 or more years—is negligible, why does the premium persist? If you are guaranteed a higher return for holding stocks at a long enough horizon, it seems to flout the efficient market hypothesis.2

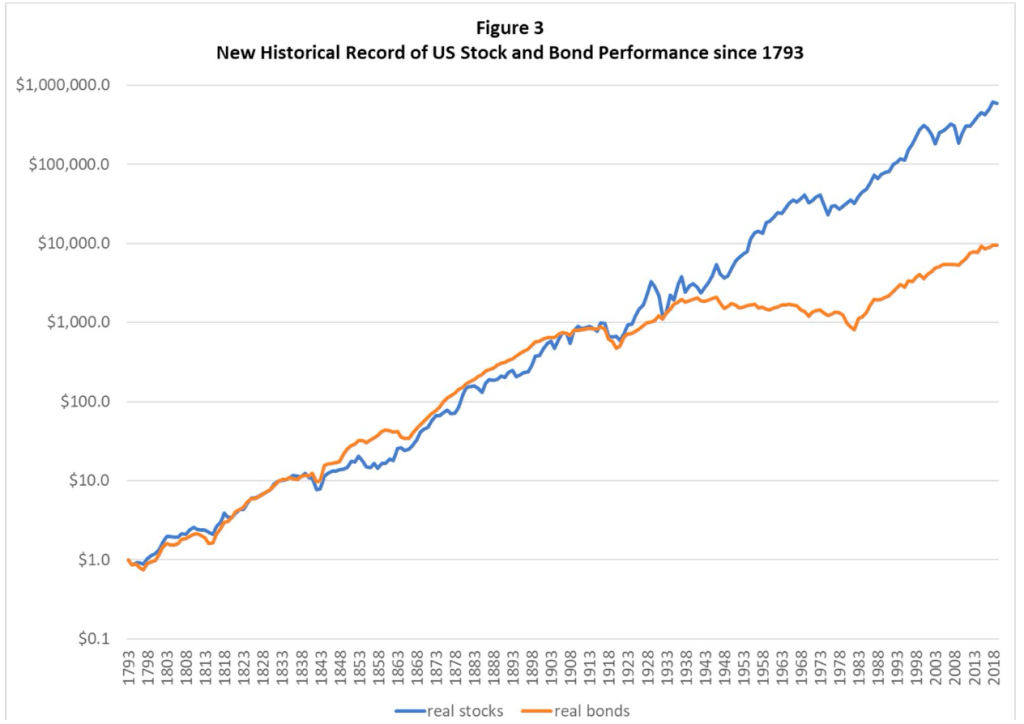

This conundrum is further complicated by the fact that the ERP was virtually non-existent prior to 1942. As I mentioned last year, research by Edward McQuarrie reconstructed much of the historical record for stocks and bonds going back to 1793. The results are somewhat troubling for investors who assume stocks always outperform bonds over long horizons.

What could cause such a divergence in stock and bond returns in the early to mid 20th Century? Why did the ERP seem to appear almost out of nowhere after nearly 150 years?

The “Ladder” and the Disaster

Some clue as to the origins of the ERP were revealed by MIT’s Lawrence Schmidt, who completed a provocative paper titled “Climbing and Falling Off the Ladder.” Schmidt’s paper implies that the ERP isn’t a reward for taking market “risk.” Instead, it is a price tag on the anxiety of the modern professional class.

Schmidt’s core argument is built on the concept of Labor Market Event Risk. Using massive datasets of administrative earnings, he shows that workers don’t just experience small fluctuations in pay; they experience “disasters”—sudden, catastrophic drops in income (the “falling off the ladder”).

Critically, these disasters are counter-cyclical and idiosyncratic. When the economy tanked in 2008 or 2020, for example, it didn’t affect everyone equally. Instead, a specific subset of people “fell off the ladder” entirely.

Schmidt examined initial unemployment claims data, demonstrating that they predict future stock returns better than almost any other indicator. He argues that, because the risk of career-ending disaster is generally “uninsurable,” investors demand a high premium to hold stocks.3 Why? Because stocks tend to crash at the exact same time their career is most likely to hit a brick wall. Stocks are a “bad hedge” for your labor income.

The Great Convergence: Worker as Capitalist

This brings us to a peculiar irony of 21st-century capitalism. In the 1800s, as McQuarrie’s data shows, the stock market didn’t consistently outperform bonds. Back then, the people owning stocks (institutions, plutocrats, rentiers and managers) and the people working the machines (the proletariat) were two entirely different groups.

In the 19th century, stocks were owned more or less as permanent investments of the uber-wealthy, paying steady dividends with little opportunity for capital appreciation. The “disaster risk” of the labor market was almost entirely borne by the worker. If a factory worker was maimed or fired, it was a tragedy, but it didn’t necessarily move the needle for a stockholder in London.4

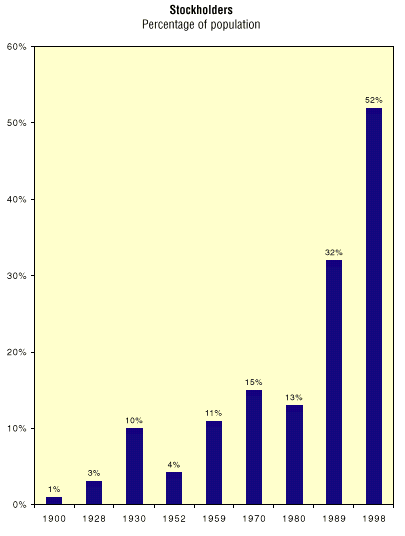

At the time, average workers and even professionals had limited opportunities to own stocks. The retail stock market wouldn’t exist in any recognizable form until after World War I. As investment trusts and eventually mutual funds became available, smaller investors were finally able to access a diversified portfolio of stocks. It was only well into the 20th century, as we moved toward a “shareholder democracy” that everyday Americans began buying stocks in droves.

Today, the “fictitious capitalist” and the “high-income laborer” are often the same person. If you are a software engineer in Seattle or a manager in Chicago, your wealth is likely tied up in a brokerage account, IRA or 401(k) full of equities. You are a “capitalist” by virtue of your savings, but a “proletarian” by virtue of your dependence on a paycheck.

Corporate shares of stock have always been a form of fictitious capital, embedded with value created by labor. But as markets have become more liquid and widely available, the risk-return profile of stocks have become even more “labor-like.”

This convergence has fundamentally changed how the market prices risk. Because the modern investor is also a worker, the stock market must pay a “bribe” (the premium) to convince that worker to put their savings into a system that is perfectly correlated with their own professional ruin.

This leads to a final irony and contradiction: As the stock market becomes more democratized, stocks offer a higher return for those who can truly hold them indefinitely (the capitalist class). But for those who are forced to sell in order fund their obligations (the precarious professional, the modest retiree and the working class), stocks offer a devil’s bargain: They may not be there when you need them most.5

So, as we look at the high returns of the last few decades, we shouldn’t just see a natural state of affairs, a reward bestowed to us by the market for “bearing the risk” of equity ownership. We should see the “dark matter” of our own professional fears. The ERP is the market’s way of pricing the fact that, in modern capitalism, we are all just one disaster away from financial ruin.

- This argument is a bit of a head scratcher; one metric for the ERP was already negative when the book was published in October, 1999. The S&P CAEY was 2.37%, while the yield on TIPS was around 3.88%, implying a -1.5% ERP. ↩︎

- Some economists retort that the risk of equities persists even at long time horizons. Investors in Russian stocks, for example, lost all their equity holdings after the 1917 Bolshevik Revolution. Similarly, between 1802 and 2023, there were at least three 75-year periods with negative real US stock returns. ↩︎

- While unemployment insurance may cover you for a short time, you can’t buy a policy against your specific career hitting a dead end. ↩︎

- This is not to say that stocks weren’t volatile. There were at least four separate bear markets in the 1800s, including one that lasted 51 years. ↩︎

- Holding a larger amount of fixed income, even at younger ages, can help insulate workers from the worst career setbacks. The standard advice—to hold 100% equities in your early working years—is fine, unless you happen to be one of the unlucky few with a multi-year layoff. Tread carefully. ↩︎

You must be logged in to post a comment.