Recently, I’ve been exploring optimal retirement asset allocations. Conventional wisdom suggests that savers should invest more conservatively as they approach retirement. The lifecycle model of investing, for example, posits that an individual’s investment strategy should change over their lifetime based on their age, financial goals, risk tolerance, and time horizon. During accumulation, investors typically have high human capital, meaning they can afford to take more risk in their investment portfolio. In retirement, this is reversed: low income potential means investors should be more conservative.

One way to do this is to match your liabilities with safe assets like bonds and leave equity investments for longer term liabilities and discretionary expenses. I briefly discussed this in a couple of posts about the longest period of stock underperformance. An initial estimate of my personal liabilities in retirement suggested that roughly a 60% stock / 40% bond allocation would fit me well–matching a common but broadly criticized benchmark.

Recently, however, the lifecycle model has come under fire from different angles, some suggesting it overweights stocks by not accounting for certain risks, while others suggest it underweights stocks by not accounting for things like mean reversion. Another set of scholarship goes even further arguing that the optimal portfolio abandons fixed income altogether. In this post, I’ll summarize some of this more recent scholarship and what it means for asset allocation.

More Bonds…

Historically, the lifecycle model has treated labor income as deterministic, possibly including permanent changes like a leave of absence or a raise, for example. However, a recent paper suggests that income risk when properly accounted for necessitates higher precautionary savings and lower stock allocations.

Sebastian Gomez-Cardona examines the risk of income shocks—meaning the positive or negative changes to worker income—in an article and companion paper at Morningstar. The paper Shocks to Income in a Lifecycle Model: An Undervalued Risk integrates income risk into financial planning by modeling labor income dynamics through deterministic trends, transitory shocks, and permanent shocks. The study finds that persistent income shocks lead investors to require higher precautionary saving rates and necessitate adjustments to their equity glide paths. The research offers practical implications by providing tailored equity allocation adjustments based on an investor’s age, wealth, and industry, advising that workers in high-risk sectors (like finance and trade) whose income is highly correlated with stock returns should maintain a lower share of equity in their financial portfolios to mitigate the combined risk.

Another paper by Edward F. McQuarrie challenges the idea that equities should necessarily outperform bonds over the long run. Where Siegel Went Awry: Outdated Sources & Incomplete Data revisits the historical record of US stock and bond performance using new digital archives that extend the data back to 1793, thereby challenging Jeremy Siegel’s thesis that stocks consistently outperform bonds over the long run, as that narrative was built upon outdated and incomplete sources. The augmented history demonstrates that the modern era (post-1926) exhibits a pattern of asset returns that does not generalize to the 19th century, during which sometimes stocks outperformed bonds, sometimes bonds outperformed stocks, and sometimes returns were similar. The author introduces a “regime thesis,” arguing that ceaseless variation exists in asset performance because both stocks and bonds should be considered risk assets.

Or Maybe More Stocks…

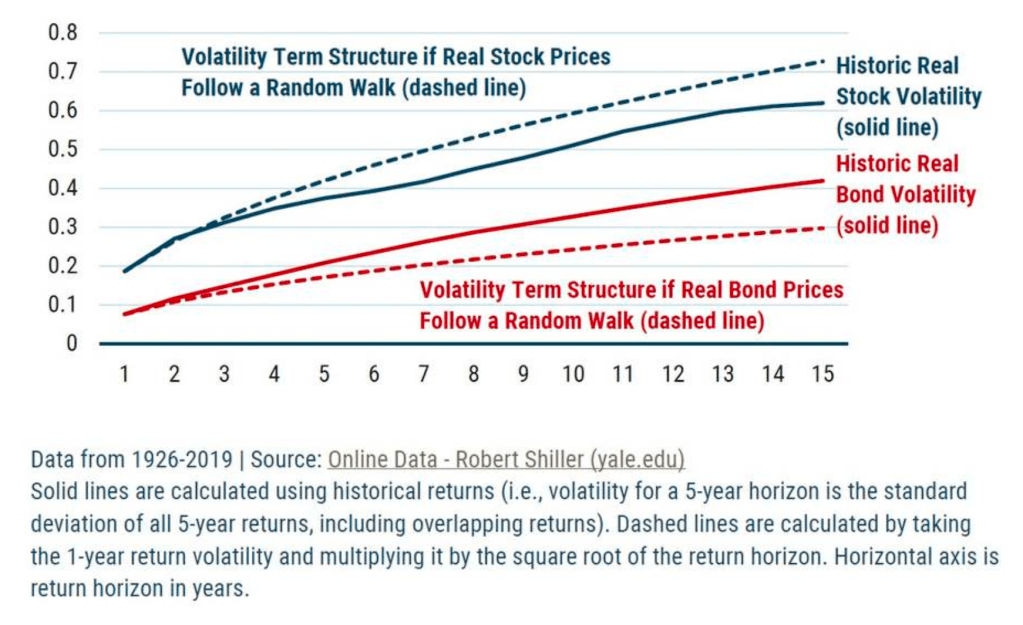

On the other hand, another author suggests that higher equity allocations can often lead to better investor outcomes. Scott Bondurant’s article Hidden in Plain Sight1 provides empirical support for the view that historical return data for stocks 1871 demonstrate mean reversion in long-term portfolios, contrasting this finding with traditional random walk (RW) methodologies. Similarly, bonds tend to “mean avert,” showing higher risk than a RW would suggest they should. The chart below shows the volatility of stocks over various terms.

The historical real stock volatility is lower than a RW would imply, while the volatility of bonds is higher. Using Monte Carlo analysis through a series of case studies, the article compares results from mean reversion (MR) models against RW models for various allocations and withdrawal rates, demonstrating that RW often underestimates the risk of ruin (i.e., the chance of going broke). The conclusion emphasizes that understanding a client’s specific situation, including the probability of success and expected drawdowns calculated using Mean Reversion analysis, is necessary for providing optimal financial advice. In many cases, depending on the particular circumstances and stock market valuation, this results in increased equity allocations.

Or Maybe No Bonds at All…

Yet another set of articles puts bond investing into question entirely. In 2023, Aizhan Anarkulova, Scott Cederburg, and Michael S. O’Doherty released “Beyond the Status Quo: A Critical Assessment of Lifecycle Investment Advice.” The paper, updated in 2025, attracted quite a bit of attention–at least enough that Ben Felix called it “the most controversial paper in finance.”

The study challenges the traditional lifecycle investment advice that investors should diversify across stocks and bonds and reduce equity allocations with age. By estimating optimal age-based weights within a lifecycle model, the authors find that the optimal asset allocation remains consistently near one-third domestic stocks and two-thirds international stocks throughout the lifecycle. The optimal age-based strategy yields higher expected utility compared to fixed-weight benchmarks (such as a 60/40 balanced portfolio or standard TDFs), demonstrating robustness across varied assumptions regarding risk aversion, bequest motives, retirement withdrawal strategies, and sample periods.

Edward F. McQuarrie and William J. Bernstein also drew the same conclusion in their recent paper Expected Outcomes of 401(k) Investing: What Can History Tell Us? This paper evaluates the demands placed on savers relying on Defined Contribution (DC) plans by testing the success requirements of periodic investments intended to fund periodic withdrawals against the historical record. The primary finding is that most savers would fail “absent inhuman levels of risk tolerance and superhuman levels of thrift.” The analysis concludes that common strategies like glide paths or balanced portfolios, while not inherently condemned, require unrealistically high savings rates (e.g., a 25% savings rate achieves high success). Meanwhile, only 100% equity portfolios fared well enough to sustain savings rates under 20%.2

The Evolving Lifecycle Model: Adjustments and Implications

I considered the studies discussed above in my own asset allocation lifecycle model. As I mentioned, the model uses bonds to cover short-term liabilities, with stocks for longer term and discretionary spending. My approach included the following modifications:

- Using historical simulation rather than a random walk Monte Carlo analysis to get a better idea of “chance of success.” This ensures that mean reversion is effectively baked into the analysis. Alternatively, if you used Monte Carlo, you could incorporate a “reversion factor” into your model.

- Incorporating the risk of “income shocks” by estimating the variance of income shocks and then reducing my estimated annual future salary by that amount in successive years. I make up for that income loss through higher allocations to bonds in the current year (providing the “future income” in case of catastrophe). This isn’t exactly how Gomez-Cardona addresses it in his paper, but it approximates the Merton Share concept of reducing risk by the square of the standard deviation.

- Diversifying beyond major asset classes into real estate, small cap value stocks, and alternatives.

- Using a valuation-aware dynamic withdrawal strategy, delaying retirement until I can guarantee a 100% historical success rate.

- Aggressively saving beyond the recommended 20% savings rate.

The papers that suggest a 100% allocation to stocks delivers the most optimal outcomes in the majority of cases may be correct, but the examination of less than stellar Antebellum stock returns in MacQuarrie’s papers give me pause. In the end, I decided it was way too risky for my taste and probably unnecessary given my high savings rate and use of a 0% historical failure rate with variable spending.

In the end, the adjustments led me back to roughly the same place I started: 60% stocks / 40% bonds (with some displacement by alts on both assets). By the time I get there though, market conditions will almost certainly have changed, so my valuation aware approach might recommend a more or less aggressive portfolio.

This is all to say that the Lifecycle Model is practically flawed and appears to be highly subjective to perceived and even currently unknown or unquantified risks. While I wouldn’t go so far as to say it is “dead,” it has been tweaked and critiqued enough to bring it into question entirely. What that means for savers, retirees and portfolio managers is difficult to say, but it certainly should give policymakers pause when considering adjustments to Defined Benefit (DB) and Defined Contribution (DC) policies.

- The subtitle of the article is a mouthful: “The Dramatic Impact on Financial Planning and Portfolio Construction When Mean Reversion Is Incorporated Into Risk and Return Expectation” ↩︎

- I have a couple of criticisms of the Anarkulova and McQuarrie articles, which I suspect could positively affect the results for most savers:

a) Both articles appear to assume a static real withdrawal rate similar to the 4% Rule. While it is a good starting point, in reality the vast majority of people have variable spending rates and many studies show that retirees underspend their assets. Most retirees have decreased liabilities in retirement (no dependents and a paid off mortgage), meaning their spending is naturally lower without negative impacts to quality of life.

b) McQuarrie and Bernstein create cohorts of savers that work and save for 30 years, then live for a remaining 30 years in retirement. While they calculate the required return for 25, 30, 35, and 40 year savings periods, the primary findings apply to 30 year savings periods only. For many workers a 30 year saving period is just too short. A worker beginning their career at age 25 would work to the age of 55, then live until age 85, longer than the current life expectancy. Studies show that the average age of retirement is more like 62. While some workers may get forced out of work early, there are few that would voluntarily give up a job if they felt they had inadequate savings, and many of them may seek part-time labor to make up any difference.

In general, I agree with McQuarrie and Bernstein that Defined Contribution programs have largely (but not entirely) failed to secure retirees’ futures by tying their success to the market and delivering outcomes that are in part based on luck. A counterbalancing reinvigorated social safety net is currently facing its own risks, and requires urgent action to reduce the impacts on seniors and future beneficiaries. ↩︎

You must be logged in to post a comment.